CacheMoola

Improving Gen Z’s understanding in the fundamentals of financial literacy.

Improving Gen Z’s understanding in the fundamentals of financial literacy.

Team

Team

Bright Hoang

Sam Lopez

Valeria Fierro

Lana Vuong

Matt Dietzman

Sophia Mai (me!)

Bright Hoang

Sam Lopez

Valeria Fierro

Lana Vuong

Matt Dietzman

Sophia Mai (me!)

Bright Hoang

Sam Lopez

Valeria Fierro

Lana Vuong

Matt Dietzman

Sophia Mai (me!)

Timeline

Timeline

34 weeks

Industry

Industry

User Research

Introduction

Introduction

CacheMoola was designed in a team of six as a eight-month long project as part of Design for America, a non-profit organization focused on using Human-Centered Design (HCD) to address real-world social challenges. My team designed a platform that serves as a resource to help Gen Z (those born between 1997 and 2012) learn more about the fundamentals of financial literacy.

CacheMoola was designed in a team of six as a eight-month long project as part of Design for America, a non-profit organization focused on using Human-Centered Design (HCD) to address real-world social challenges. My team designed a platform that serves as a resource to help Gen Z (those born between 1997 and 2012) learn more about the fundamentals of financial literacy.

Results

Results

We have not completed this project yet! Check back for updates :)

We have not completed this project yet! Check back for updates :)

Gen Z's Financial Struggles

Despite representing approximately a quarter of the workforce, a recent WalletHub survey found that more than one-quarter of Gen Z admits to lacking confidence in their financial knowledge, making them the least financially confident generation. This can be seen in Gen Z’s spending and investing habits: 57% of Gen Z individuals prefer a savings account as their go-to investment method. Not being financially literate can lead to poor financial decisions, leading to debt and financial instability.

Gen Z's Financial Struggles

Despite representing approximately a quarter of the workforce, a recent WalletHub survey found that more than one-quarter of Gen Z admits to lacking confidence in their financial knowledge, making them the least financially confident generation. This can be seen in Gen Z’s spending and investing habits: 57% of Gen Z individuals prefer a savings account as their go-to investment method. Not being financially literate can lead to poor financial decisions, leading to debt and financial instability.

Competitive Analysis

We began this project by brainstorming ideas of ways to teach Gen Z about financial literacy (ie. TikTok/short-form content, games, etc.). Based on this brainstorm, we looked into competitors that were involved with financial literacy, education in general, or both to get a good understanding of any gaps that our product could fill.

Competitive Analysis

We began this project by brainstorming ideas of ways to teach Gen Z about financial literacy (ie. TikTok/short-form content, games, etc.). Based on this brainstorm, we looked into competitors that were involved with financial literacy, education in general, or both to get a good understanding of any gaps that our product could fill.

SWOT Analysis

SWOT Analysis

Takeaway #1

Takeaway #1

It's hard to verify the credibility of online sources.

Educational competitors (ie. TikTok, Youtube, AI, in-person workshops, classes) are effective, but there's a lot of conflicting/wrong information, which can make people confused. There also may be issues about sharing private financial information to AI and limited accessibility to in-person resources.

It's hard to verify the credibility of online sources.

Educational competitors (ie. TikTok, Youtube, AI, in-person workshops, classes) are effective, but there's a lot of conflicting/wrong information, which can make people confused. There also may be issues about sharing private financial information to AI and limited accessibility to in-person resources.

Takeaway #2

Takeaway #2

Many financial literacy resources not accessible for beginners.

Existing apps/resources (ie. Wealthfront, Nerdwallet) were designed mostly for those with more knowledge about financial literacy and contain a lot of jargon, which can be confusing for those with little/no prior knowledge.

Many financial literacy resources not accessible for beginners.

Existing apps/resources (ie. Wealthfront, Nerdwallet) were designed mostly for those with more knowledge about financial literacy and contain a lot of jargon, which can be confusing for those with little/no prior knowledge.

Takeaway #3

Takeaway #3

Apps targeted at beginners/Gen Z often lack helpful content/limit possible engagement for users.

These apps are usually gamified to make them engaging for users, but don't actually teach financial literacy concepts.

Apps targeted at beginners/Gen Z often lack helpful content/limit possible engagement for users.

These apps are usually gamified to make them engaging for users, but don't actually teach financial literacy concepts.

Surveys

To gain a general understanding of our target users' pain points, current experiences, and wants, our team conducted one round of surveys. We reached out to people of different ages (within Gen Z’s constraints) and backgrounds to gauge Gen Z’s general understanding of financial literacy.

Methods

We used Google Forms as our survey tool and posted the link on social media (Instagram, Snapchat, Reddit, Slack), in order to share our survey to a larger audience, as well as distribute our survey to people over Winter Break.

Ideal participants for this survey are Gen Z (born 1997-2010). We wanted a broad range of perspectives on financial literacy within Gen Z, so we wanted to include people of all racial, ethnic, economic, and immigration backgrounds.

Surveys

To gain a general understanding of our target users' pain points, current experiences, and wants, our team conducted one round of surveys. We reached out to people of different ages (within Gen Z’s constraints) and backgrounds to gauge Gen Z’s general understanding of financial literacy.

Methods

We used Google Forms as our survey tool and posted the link on social media (Instagram, Snapchat, Reddit, Slack), in order to share our survey to a larger audience, as well as distribute our survey to people over Winter Break.

Ideal participants for this survey are Gen Z (born 1997-2010). We wanted a broad range of perspectives on financial literacy within Gen Z, so we wanted to include people of all racial, ethnic, economic, and immigration backgrounds.

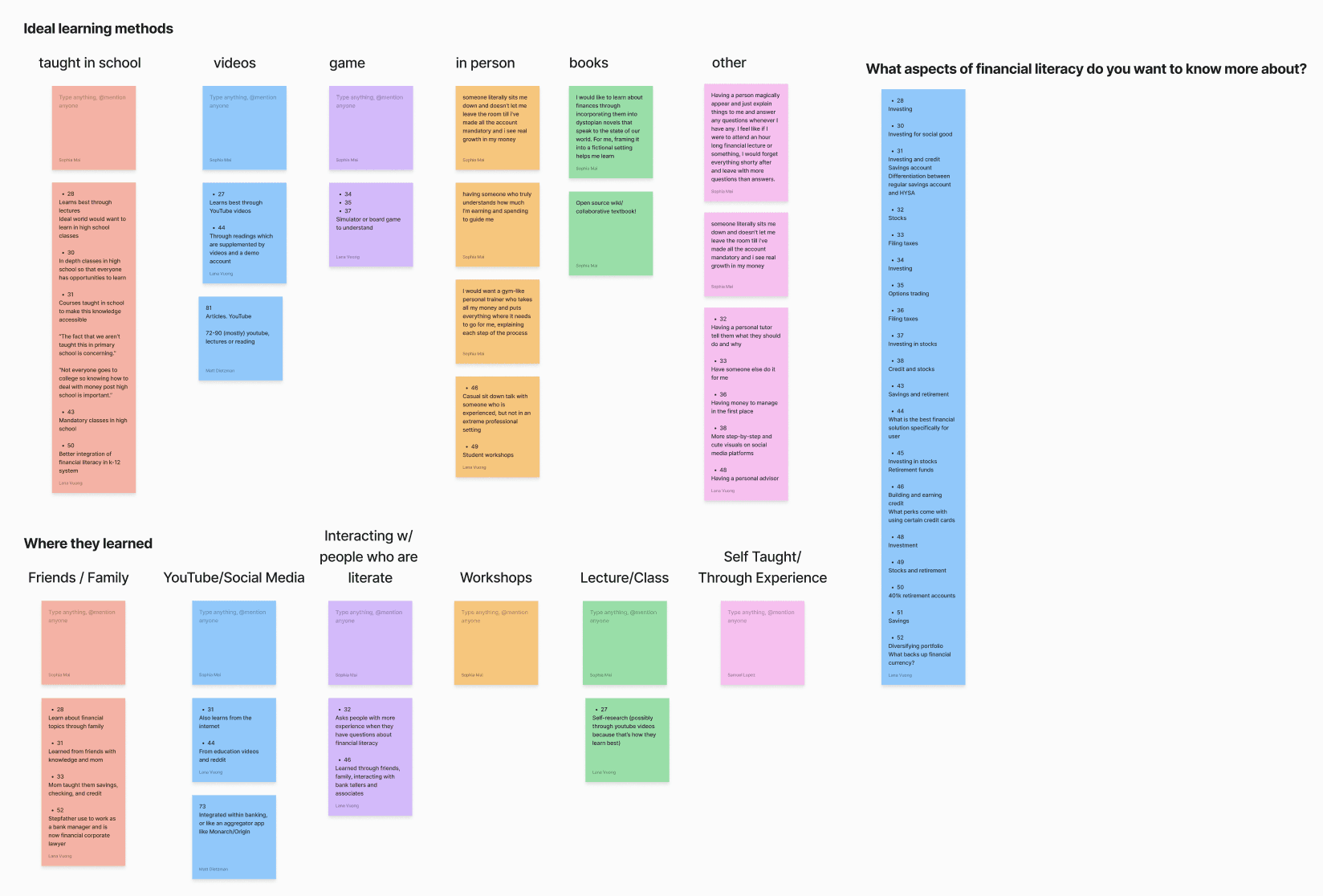

Key Survey Questions

Key Survey Questions

Rate your overall level of personal financial literacy

What is your familiarity with these products/concepts (checking account, savings account, high-yield savings account, credit, retirement account, investing in stocks, filing taxes), and have you used them before?

Rate your comfort level with the following topics: savings, high-yield savings account, credit, retirement, investing in stocks, filing taxes?

How did you learn about the topics above?

What mediums do you learn best from?

What aspects of financial literacy do you want to learn more about?

What has discouraged you from learning about financial products/services in the past?

In an ideal world, how would you want to learn about personal finances? (Tell us your most creative and craziest answers!)

Rate your overall level of personal financial literacy

What is your familiarity with these products/concepts (checking account, savings account, high-yield savings account, credit, retirement account, investing in stocks, filing taxes), and have you used them before?

Rate your comfort level with the following topics: savings, high-yield savings account, credit, retirement, investing in stocks, filing taxes?

How did you learn about the topics above?

What mediums do you learn best from?

What aspects of financial literacy do you want to learn more about?

What has discouraged you from learning about financial products/services in the past?

In an ideal world, how would you want to learn about personal finances? (Tell us your most creative and craziest answers!)

Affinity Map

Takeaway #1

Takeaway #1

Participants were generally not very knowledgeable about financial literacy.

Most indicated that they were not familiar enough to teach others/were uneducated.

People often learned their current financial literacy knowledge from friends, family, and people they know that are more familiar than they are.

Participants were generally not very knowledgeable about financial literacy.

Most indicated that they were not familiar enough to teach others/were uneducated.

People often learned their current financial literacy knowledge from friends, family, and people they know that are more familiar than they are.

Takeaway #2

Takeaway #2

Participants were less knowledgeable about investing, retirement, & filing taxes and wanted to learn more about them.

People were more knowledgeable about checking, savings, & credit.

Participants were less knowledgeable about investing, retirement, & filing taxes and wanted to learn more about them.

People were more knowledgeable about checking, savings, & credit.

Takeaway #3

Takeaway #3

Most common discouraging factors:

Overwhelming

Intimidating

Lack of resources (ie. money, time, & not accessible)

Most common discouraging factors:

Overwhelming

Intimidating

Lack of resources (ie. money, time, & not accessible)

Takeaway #4

Takeaway #4

Most popular preferred learning methods:

Taught in school (preferably high school)

Someone to walk them through it & answer questions

Videos.

Most popular preferred learning methods:

Taught in school (preferably high school)

Someone to walk them through it & answer questions

Videos.

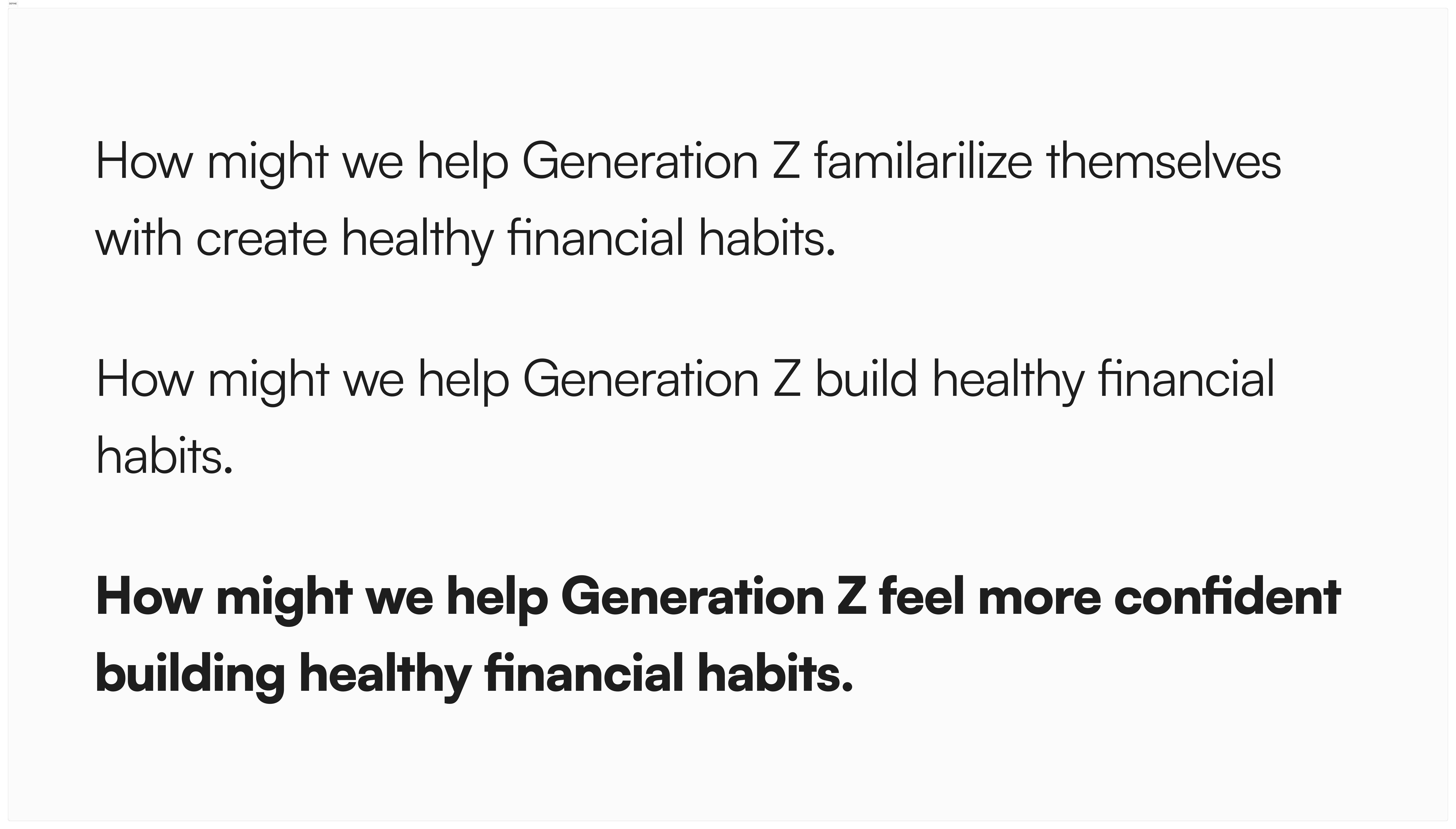

Defining & Refining Our Problem Statement

Initial Problem Statement: How might we design a resource that teaches Gen Z the fundamentals of personal financial literacy so they can be comfortable with budgeting, building credit, investing, etc.?

Upon conducting competitor research and surveys, we narrowed our scope to make our problem statement more specific and honed in on the concepts users indicated that they wanted to learn more about.

Because many participants of our survey indicated that they wanted to build better financial habits, we wanted to focus on fostering that through our solution.

Defining & Refining Our Problem Statement

Initial Problem Statement: How might we design a resource that teaches Gen Z the fundamentals of personal financial literacy so they can be comfortable with budgeting, building credit, investing, etc.?

Upon conducting competitor research and surveys, we narrowed our scope to make our problem statement more specific and honed in on the concepts users indicated that they wanted to learn more about.

Because many participants of our survey indicated that they wanted to build better financial habits, we wanted to focus on fostering that through our solution.

Interviews

To better understand people's pain points, current experiences, and wants, our team conducted four interviews. To recruit interviewees, we reached out to people who volunteered to be interviewed after taking our survey.

We wanted to gain more thorough information about what barriers prevented members of Gen Z from learning about financial literacy, and how to tackle those challenges.

Methods

We reached out to people who took our survey and volunteered to be interviewed.

We focused on members of Gen Z and those who are not very familiar with financial literacy in order to gain more insight into why they have not learned more about financial literacy, and what ways we can tackle those issues in our solution.

We conducted these surveys in-person to create a better connection and establish more trust for our participants.

Interviews

To better understand people's pain points, current experiences, and wants, our team conducted four interviews. To recruit interviewees, we reached out to people who volunteered to be interviewed after taking our survey.

We wanted to gain more thorough information about what barriers prevented members of Gen Z from learning about financial literacy, and how to tackle those challenges.

Methods

We reached out to people who took our survey and volunteered to be interviewed.

We focused on members of Gen Z and those who are not very familiar with financial literacy in order to gain more insight into why they have not learned more about financial literacy, and what ways we can tackle those issues in our solution.

We conducted these surveys in-person to create a better connection and establish more trust for our participants.

Key Interview Questions

Key Interview Questions

Rate your overall level of personal financial literacy?

Why did you give that rating?

What financial products/services do you use?

What do they do?

Why do you use them?

Who taught you to use them?

How do you use them?

What obstacles have you encountered while trying to learn about financial literacy?

Why were they obstacles?

What existing resources have you used?

Why haven’t they worked for you?

how do you think they can be improved?

What financial products/services do you want to learn more about?

Why do you want to learn more about them?

What are your short & long term financial goals?

How do you think learning about financial literacy will help you reach your goals?

How would you want to learn about financial literacy in the future?

What would help you learn & why?

What detracts from your learning?

Rate your overall level of personal financial literacy?

Why did you give that rating?

What financial products/services do you use?

What do they do?

Why do you use them?

Who taught you to use them?

How do you use them?

What obstacles have you encountered while trying to learn about financial literacy?

Why were they obstacles?

What existing resources have you used?

Why haven’t they worked for you?

how do you think they can be improved?

What financial products/services do you want to learn more about?

Why do you want to learn more about them?

What are your short & long term financial goals?

How do you think learning about financial literacy will help you reach your goals?

How would you want to learn about financial literacy in the future?

What would help you learn & why?

What detracts from your learning?

Affinity Map

Affinity Map

Ideation

Based on our insights for our user research, we wanted to focus on several key aspects for our product:

Educate users about stocks

Create ways for users to build healthy habits

Make financial literacy more accessible (less overwhelming & intimidating)

With these main ideas in mind, we created sketches, shown below.

Ideation

Based on our insights for our user research, we wanted to focus on several key aspects for our product:

Educate users about stocks

Create ways for users to build healthy habits

Make financial literacy more accessible (less overwhelming & intimidating)

With these main ideas in mind, we created sketches, shown below.

Brainstorming Sketches

Brainstorming Sketches